Nigeria’s Kaduna state declares ‘tomato emergency’

A state of emergency has been declared in the tomato sector in Kaduna state, northern Nigeria, local media report.

A moth called the Tomato Leaf Miner, or Tuta Absoluta, has ravaged 80% of tomato farms, Commissioner of Agriculture Daniel Manzo Maigar said. He said 200 farmers together lost at least 1bn naira ($5.1m; £3.5m) over the past month.

The price of a basket of tomatoes has increased from $1.20 less than three months ago to more than $40 today.

In Nigeria, officials declare a state of emergency to indicate they are taking drastic action to deal with a problem, the BBC’s Muhammad Kabir Muhammad says.

In this case the state sent government agricultural officials to Kenya to meet experts on the Tomato Leaf Miner to learn how to deal with the pest.

Kaduna is in the north of the country, where according to the UN most tomato production takes place,

A tomato paste manufacturing business in northern Kano state owned by Africa’s richest man, Aliko Dangote, suspended production earlier in the month due to the lack of tomatoes, reports Forbes.

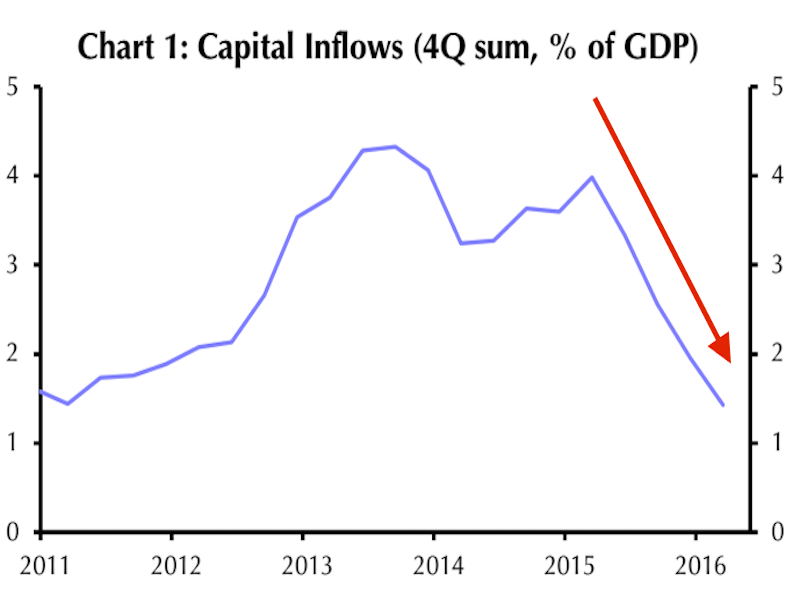

Africa’s largest oil producer just took another huge blow to its battered economy

“Many investors are waiting for the naira to be devalued towards something closer to the parallel market rate.”

The flow of foreign capital into Nigeria is drying up — and it’s a huge blow to its economy.

Foreign investments into Africa’s biggest oil producer came in at $711 million in the first quarter of 2016 — a whopping 74% drop from a year before.

The steepest decline came from portfolio inflows, which dropped 85% year-over-year, according to analysts at Capital Economics.

“The collapse in investment inflows will deal two very serious blows to Nigeria’s economy, which is already reeling due to low oil prices,” warned Capital Economics’ Africa economist, John Ashbourne, in a note to clients.

“This will exacerbate the country’s serious balance of payments problems and further depress investment in an economy that is starved of capital,” he continued.

Notably, although it’s easy to point the finger at lower oil prices, that’s not the only thing souring sentiment toward Nigeria. Many investors have also been discouraged by the government’s controversial policies.

Recently, the government has pursued an agenda of currency and price controls — including on petrol — which has resulted in inflation soaring to its highest rate since July 2012 and in one of the worst fuel shortages in years.

The “complex FX restrictions caused Nigeria to be ejected from a widely-tracked JPMorgan EM bond index in Q3 2015 and have deterred potential investors who worry about repatriating earnings,” added Ashbourne. “Many investors are waiting for the naira to be devalued towards something closer to the parallel market rate.”

In short, it’s not looking great.

One year ago, Buhari promised to change Nigeria

Buhari still has adequate time to turn his fortunes around, but he must be wary of the kind of executive arrogance that undid Jonathan’s party and government.

When Nigerians rouse from sleep on April 1, they will again head for filling stations to join the now de rigueur queues for Premium Motor Spirit.

By Fisayo Soyombo

This is no big news; queueing for hours at petrol stations has been the most recurring item on the itinerary of Nigerians not only for the past month, but also for the third spell in the past three months.

What is news is that when these same people woke up exactly one year ago, the majority of them trooped to the streets in jubilation. Three hours and 47 minutes into that day, opposition candidate Muhammadu Buhari was declared president-elect.

But while Nigerians hailed Buhari as a Messiah of sorts, they forgot to remind themselves that no Nigerian leader, democratic or dictatorial, had ever succeeded in delivering socioeconomic prosperity to the masses.

Joy so often short-lived

There was something familiar about the sheer joy that was unleashed on the streets of Nigeria on April 1, 2015.

More than five decades ago, on October 1, 1960, when Sir Abubakar Tafawa Balewa accepted the symbols of Independence from the Queen of England and cheerily declared that he was “opening a new chapter in the history of Nigeria”, it was to the delight of millions of citizens.

Elites clutched at their radios as devout Catholics would the Rosary, listening as the sonorous voice of Emmanuel Omatsola blared from Race Course, Lagos: Nigeria is a free, sovereign nation. Pupils holidayed; and when they returned to school, they were served unusual rounds of sumptuous meals and handed lovingly petite green-white-green flags.

But for all of Balewa’s education and popularity in international circles, his reputation for championing northern interests did little to foster unity and stability in Nigeria’s delicate multiethnic set-up. Both power and life were taken away from him in a coup six years later.

When Nigeria returned to democracy in 1999, after decades of torture at the hands of the military, the scenarios were repeated. Olusegun Obasanjo, a retired soldier who was on the throes of death in prison, was suddenly, miraculously handed democratic power.

Obasanjo had admitted that “the entire Nigerian scene is very bleak indeed, so bleak people ask me: where do we begin?” But he also promised to fight corruption, restore public confidence in governance, build infrastructure. Millions of overjoyed Nigerians believed him – the worst civilian government is better than the best military regime was the popular reasoning at the time.

In his book, This House Has Fallen, published a year into Obasanjo’s presidency, British journalist Karl Maier had written: “The government spends up to half its annual budget on salaries of an estimated two million workers… yet the civil service remains paralysed, with connections and corruption still the fastest way to get anything done. Up to 75 percent of the army’s equipment is broken or missing vital spare parts. The Navy’s 52 admirals and commodores outnumber serviceable ships by a ratio of six to one. The Air Force has 10,000 men but fewer than 20 functioning aircraft.”

Sixteen long years later, it is heartbreaking to see that these are still some of the issues dominating Nigerian political discourse.

Gloom of Buhari’s victory

Caveat: this is not an appraisal of Buhari’s reign – not yet. But some of his first words as president-elect back in 2015 were: “You voted for change and now change has come.”

Goodluck Jonathan’s presidency ended with a biting fuel scarcity that suffering masses felt would accompany Jonathan out of office. On the anniversary of Buhari’s victory, that scarcity they so despised is exactly what they’re grappling with. There are no noticeable improvements in erratic power supply, the unhealthy economy, the dearth of jobs. No “change”, really.

Buhari still has adequate time to turn his fortunes around, but he must be wary of the kind of executive arrogance that undid Jonathan’s party and government.

It is the same type of arrogance that made Minister of State for Petroleum, Ibe Kachikwu, declare in the face of the ongoing petrol scarcity: “One of the trainings I did not receive was that of a magician.” Only to tell prospective protesters days later: “Save your fuel, I am not going to resign” is dangerous.

That Femi Adesina, Buhari’s spokesman, told Nigerians a day earlier that: “If some people are crying that they are in darkness, they should go and hold those who vandalise the installations” betrays Buhari’s administration’s intolerance of criticism and suggests possible abdication of leadership.

Just in case Buhari has forgotten, in May, when he will have completed a quarter of his term in office, Nigerians will not only be carefully assessing the state of his “change” agenda, they will also be wondering if his party deserves to be retained in 2019.

Fisayo Soyombo edits the Nigerian online newspaper TheCable.

Nigeria’s import curbs drain life from bustling Lagos ports

Apapa Port Terminal

Maggie Fick | Financial Times /

Nigeria’s Apapa port is usually a frenetic place, where ships line up for days to offload imports ranging from used cars and plywood to rice, frozen fish and champagne. Snaking queues of trucks are usually waiting for the cargo. But the busiest port in Africa’s biggest economy has become eerily tranquil in recent months. Even the women who sell lunches of soup and pounded yams to customs officers and dock workers have mostly stopped turning up.

“Apapa is so empty now that in the evenings you will find security guards playing football in the container yards,” says a frustrated clearing agent at the port, a sprawling site in Nigeria’s commercial capital Lagos that sits near the mouth of the lagoon from which the city gets its name. The country’s top shipping executives and customs officials voice similar concerns.

To stem an ongoing fall in foreign reserves caused by the oil price crash, Nigeria’s central bank introduced restrictions last summer that have effectively blocked imports of hundreds of items that typically enter Nigeria through its ports.

The policy, backed by President Muhammadu Buhari, also aims to boost local manufacturing and agriculture. The country has long used its oil revenues to bring in essential items such as steel and palm oil that the Buhari administration says should be made locally.

Yet in the short term the policy is forcing local manufacturers to cut operations and lay off workers because they cannot import the raw materials they need to make goods.

Nigeria is already suffering its worst economic slowdown in 15 years due to the oil price fall that began in mid-2014. Shipping industry executives are warning the sharp drop in imports will add to the woes.

“We’re feeling the pressure now with our import volumes down, but all aspects of the economy are interrelated and these heavy restrictions are causing more uncertainty”, says Val Usifoh, chairman of the Shipping Association of Nigeria. The association represents the international companies handling most of the container trade in Nigeria, including Danish shipping giant Maersk and France’s CMA CGM.

One Lagos-based shipping executive notes that the companies operating the terminals at Apapa and Tin Can Island, the other main port in Lagos, have collectively laid off several thousand workers in recent months.

Nigeria’s national assembly last month passed a high-spending budget that aims to stimulate the slowing economy and diversify away from oil. The budget, which still needs a final sign-off from Mr Buhari, proposes that one way to make up for lower oil revenues is to boost tax and customs takings — but executives and some government officials say the drop in imports could derail this plan.

“The ports are nearly empty and customs revenue is nowhere close to where it should be”, says a senior manager at a port operator. Arrivals of vessels importing steel are down by about 60 per cent, he adds.

An executive at a company that processes imports says arrivals handled by his group were down 20 per cent in the first quarter of this year, compared with a year ago.

Apapa Port …the busiest port in Africa’s biggest economy has become eerily tranquil in recent months.

Some trade was being rerouted through Cotonou port in neighbouring Benin and brought into Nigeria via land borders, where customs duties are lower and therefore generate less money for the government, he says. He and other businessmen point out that smuggling — an age-old problem in Nigeria — is an obvious result of the blocking of the main entry point for the country’s imports.

Nigeria’s customs agency aims to make 1tn naira ($5bn) in revenues this year, well below the amount targeted by the federal inland revenue service, which wants to rake in $25bn. But every bit of extra non-oil revenue counts. The country’s budget deficit this year is about $15bn.

Hameed Ali, head of the customs agency, was quoted in the local press this month as saying quarterly customs revenues were down because of the import restrictions. The head of the ports authority also said the restrictions were slowing business at the ports, according to local media reports.

Despite the significant decrease in import volumes, “customs revenue might remain stable” if the Nigeria Customs Service cuts down on the graft embedded in the system, says Kayode Akindele of the Lagos-based investment firm TIA Capital. “A lot has gone missing in the past.”

Mr Usifoh says the one “glimmer of hope” for shippers is that exports have picked up slightly in recent months. But this has not yet improved the spirits of the clearing agents who rely on being paid to process a steady stream of incoming containers.

“We can only pray to God”, says one. Sitting at her desk sweating amid a power cut on a recent morning in Apapa, she directs her ire at the president, snapping: “He said he’d perform miracles within a second.”

Nigeria Revenue Drops to 5-Year Low as Tax, Oil Income Fall

Nigeria’s revenue fell last month to the lowest level in more than five years as taxes and oil earnings dropped, making it more difficult for the government of Africa’s largest economy to pay public workers.

The country’s federal, state and local governments were altogether allocated 300 billion naira ($1.5 billion) in March, the Ministry of Finance said in a statement e-mailed late Thursday from the capital, Abuja. To assist the lower-tier governments, the ministry also waived 10.9 billion naira of loan repayments.

About 27 of 36 states are “currently experiencing challenges meeting their salary payments,” the ministry said. “We are not able to guarantee that all states will be able to meet their salary obligations.”

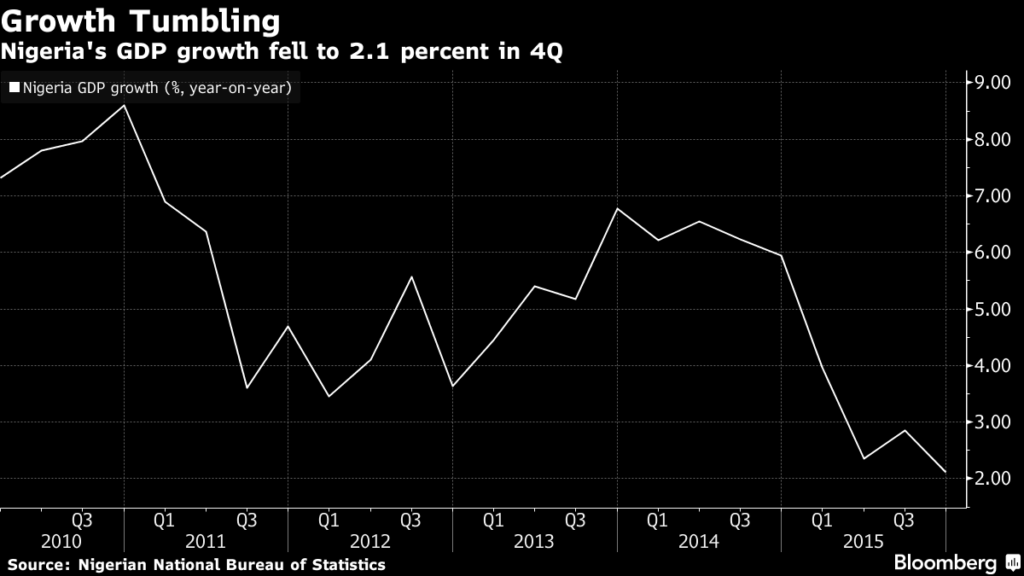

Nigeria, Africa’s biggest oil producer, has been hammered by crude prices falling 60 percent since mid-2014 to about $45 a barrel. The economy grew 2.8 percent last year, the slowest since 1999. That pace will probably falter further to 2.3 percent in 2016, the International Monetary Fund said last month.

A decision by the government in the nation of 180 million people to peg its currency even as oil revenue falls has been blamed by analysts for worsening the crisis. Foreign investors are shunning the country’s bonds and stocks until there’s a devaluation, while local businesses are struggling to import essential raw materials.

“This is another by-product of a broken foreign exchange policy,” Alan Cameron, an economist at Exotix Partners LLP in London, said by phone on Friday. “Unpaid civil service salaries have the potential to turn into a big social and political problem because for every salary paid there are likely to be several more people who rely on it.”

The central bank has kept the naira’s official rate at 197-199 against the dollar since March 2015, causing a rationing of foreign exchange to businesses which has led to shortages of goods from gasoline to milk and has sent the local currency plunging to 320 on the black market.

Not Convinced

President Muhammadu Buhari, 73, has made it clear that he, not the central bank, has the final say on currency policy — and that he is against devaluation just as he was during his first stint in power as a military ruler in the 1980s. The former general is loath to be seen by voters as capitulating to foreign investors and the IMF, both vocal critics of his stance.

Buhari reiterated on Friday that he has yet to be convinced that a weaker naira will have any tangible benefit to most Nigerians in the import dependent country. He said in a statement that a previous devaluation after he was deposed in a 1985 coup didn’t lead to the creation of jobs or new industry.

“When I was military head of state, the IMF and the World Bank wanted us to devalue the naira,” Buhari said. “But I stood my ground for the good of Nigeria.”

Nigeria’s new start is in danger of derailing – Financial Times

President Muhammadu Buhari submits his budget for 2016 to the Senate chamber (file photo)

Nigeria’s journey from bankrupt, pariah state to Africa’s largest economy helped to fuel a surge in optimism about the continent over the past 15 years. Now there is a danger that its latest troubles will trigger a bout of despair. As one seasoned investor puts it: “Nigeria, with help from South Africa, is killing the African story.”

Part of that story was hyperbole — notably the broad-based nature of the continent’s revival. While there was a boom in services, investment flows and an expansion of the middle class, growth in many states was largely jobless, and underpinned by soaring world prices for commodity exports. This was especially true in Nigeria, which still depends on crude oil for more than 90 per cent of hard currency earnings and typically around two-thirds of state revenues.

Since thefall in oil prices, the cracks in Nigeria’s economy have quickly reappeared. Starved of fuel, electricity and foreign exchange the economy is grinding to a halt. Businesses are laying off staff in droves.

In turn, confidence in President Muhammadu Buhari, elected a year ago on a wave of hope, is evaporating. There are no easy answers to the dilemmas his government faces. Many were in the making long before he won elections, promising to crush corruption,invest in infrastructureand create jobs.

The challenge is exemplified by the fuel crisis — the worst in living memory. Because state-owned refineries have been mismanaged for so long, Nigeria relies on imports of fuel. This is one reason Mr Buhari is so reluctant to devalue the naira currency — fixed at an unrealistic level against the dollar, which does not fluctuate with Nigeria’s changing fortunes. The resulting distortions have eroded the commercial case for importing fuel and created a gaping spread between parallel and official exchange rates that encourages the very corruption Mr Buhari has vowed to stop.

Devaluation would be no panacea. It would hasten the depletion of foreign reserves and push up the pump price of petrol, unless government resumes paying subsidies it can ill-afford. The elimination of the subsidy might, on the other hand, trigger riots.

It is a tough choice and an even tougher political environment to make it in. Nigerians are impatient for the gains they voted for and have little appetite for further pain. Mr Buhari squandered an opportunity to act early on when he enjoyed the goodwill of the public. But the painful measures required to set Nigeria’s economy on a sustainable growth path become no more palatable the longer he delays.

Without investment Nigeria will neither continue growing nor diversify from its crippling dependency on oil. Yet no investor will put money into an economy at one exchange rate, knowing that to take it out again might require losing a third of its dollar value.

This week, China has offered help with a currency swap, and the promise of $6bn in infrastructure loans. The terms of these deals are not yet clear. But they could go some way towards plugging an $11bn budget deficit. The danger is that, together with the modest recent rise in oil prices, China’s help will encourage Mr Buhari to defer the tough decisions once again.

The president wants to eliminate the wasteful patronage on which venal elites have thrived and create an economy more dynamic in creating jobs for the masses. These are laudable long-term aims for which his government has yet to articulate a convincing strategy. In the meantime, however, the short term is pressing. No economy can survive without fuel, electricity or foreign exchange.