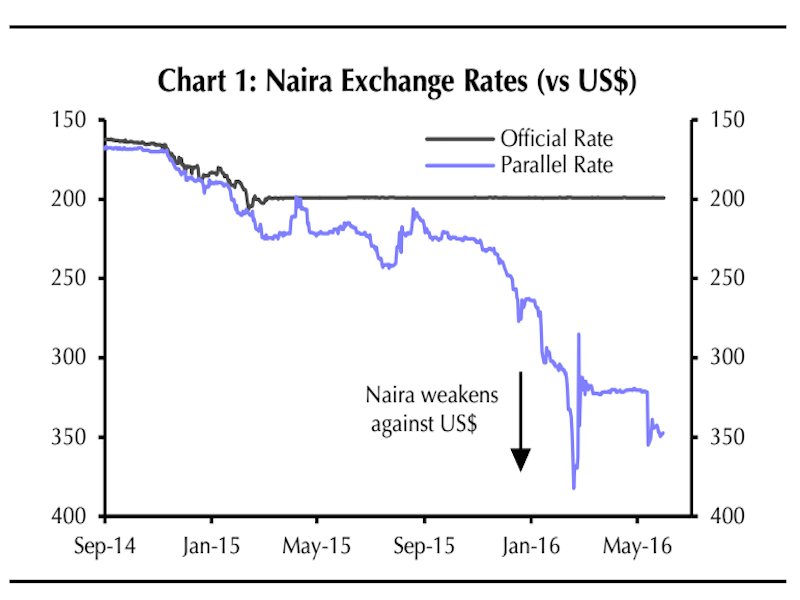

The Nigerian naira just dipped past 300 per dollar for the first time ever. The currency weakened by 2.3% to 300.25 per dollar around 8:41 a.m. ET, according to data from Bloomberg. The naira is trading around 296.50 per dollar as of 9:51 a.m. ET, according to Investing.com’s data. Back in late June, the Central Bank of Nigeria finally unpegged the naira from the US dollar, which sent the currency down by 30% to about 280 per dollar. It was pegged around 197-198 per dollar. Notably, some analysts and economists have noted in recent weeks that the currency is looking a lot less “free” than was promised last month, and had argued that the currency probably needed to fall below 300 per dollar. (Investing.com) As for the rest of the world, here’s the scoreboard as of 9:41 a.m. ET:

The British pound is down by 1.0% at 1.3096 against the dollar after some ugly data. Composite reading for Markit flash PMI fell to 47.4 in June, its lowest reading since March 2009. Additionally, manufacturing PMI sank to a 44-month low of 49.1 and services PMI tumbled to an 87-month low of 47.4. All three readings were below the 50.0 level, which theoretically indicates a contraction. “This spooked understandably spooked investors and sent the pound tumbling,” wrote Business Insider’s Will Martin.

The euro is little changed at 1.1016 against the dollar as the eurozone economy showed “surprising resilience” after the Brexit vote. The Markit PMI composite reading came in at 52.9 for June, down slightly from May’s reading of 53.1 but ahead of the 52.5 that economists were forecasting. Germany’s services sector impressed with a print of 54.6, while its manufacturing sector disappointed with a reading of 53.7. Readings in France impressed across the board, but the manufacturing sector remained in contraction at 48.6, a four-month high.

The US dollar index is little changed after Markit flash manufacturing PMI rose to an 8-month high. Separately, the Baker Hughes rig count will be out at 1 p.m. ET.

The Japanese yen is little changed at 105.95 per dollar.

Nigeria: The oil crash has people worried about a new banking crisis

Speaking to reporters on Monday, the central bank’s governor, Godwin Emefiele, asserted that Skye Bank “is not in distress and remains a healthy bank in the system.” And on Wednesday, the central bank said that all its banks are safe, and that “there is, therefore, no need for panic withdrawals from any bank,” according to Bloomberg’s Wallace.

However, these comments haven’t been enough to alleviate worries about the rest of the country’s banking system.

“This development may raise fears about the health of Nigeria’s entire banking sector; especially given the weak economic growth expected in 2016 (we forecast just 0.8% GDP growth this year),” Bank of America Merrill Lynch’s Africa economist Oyin Anubi wrote in a note to clients on Wednesday.

The Central Bank of Nigeria announced earlier this week that it’s replacing the management of the country’s eighth biggest lender by assets, Skye Bank, after it failed to meet the minimum capital ratios, according to Bloomberg’s Emele Onu, Renee Bonorchis, and Paul Wallace.

Data from the Nigerian Bureau of Statistics released in late May revealed that the country’s economy shrank way more than expected in the first quarter — by 0.4% year over year. Analysts promptly warned that these numbers suggested the country is headed for a “full-blown economic crisis.”

Banks in particular have been feeling the pain from the oil sector slump, given that the sector gives about 26% of its loans to oil and gas companies, according to December 2015 data cited by Anubi.

Notably, in this environment, Anubi argued that nonperforming loans are “likely to continue the upward trend on weak growth.” Here’s what he wrote in his note to clients (emphasis ours):

“In the course of 2016, it is likely that a significant part of the rise in NPLs will be due to problem loans in the oil sector. Some banks have been proactive in this arena. In December 2015, Moody’s claimed that 20% of oil and gas loans had already been restructured with maturity extensions and we expect that these activities have continued this year. However, there is a possibility that the downturn in the oil and gas sector (and in the overall economy) seen so far this year is worse than the banks anticipated, implying that there could be more pain ahead.

“The operating environment in Nigeria is difficult. In S&P’s most recent review of the sector the rating outlook was revised to negative for six banks, mainly due to low oil prices, weak growth, FX shortages, higher cost of risk, liquidity pressures and falling asset quality. They expect NPLs to rise to 6.0% in 2016 from 5.5% in 2015, above the prudential CBN ceiling of 5.0%. Data from Q16 results of the largest banks shows average NPLs of 7.0%. History shows that lower oil prices tend to lead to higher NPLs. However, this time, the recovery in oil prices will to some extent be offset by lower oil production.”

As for Skye Bank, its market value has plunged by more than 85% over the past five years and is down about 40% in 2016 alone, according to Bloomberg.

The central bank had deemed Skye Bank “systemically important,” but, as Anubi points out, “this bank is only 4% of total industry assets. Nigeria’s larger banks look better capitalized.”

According to local press reports cited by Anubi, most of Nigeria’s larger banks have stronger capital adequacy ratios than Skye Bank. The latter’s is reportedly below the 15% minimum requirement, while other large banks are, on average, at 19.9%.

In any case, Nigeria’s banking system might be something to keep an eye on.

Derivatives as a risk management tool in Nigeria

By Kingsley Ughe, Esq.

Risk management is one of the most fundamental aspects of business growth. The use of derivatives in corporate risk management has grown exponentially in the last decade and has transformed global financial markets, fuelled in part by the success of the financial industry in creating a variety of over-the-counter (OTC) and exchange-traded products.

Derivatives are financial instruments, which derive their value over time from an underlying asset. Assets that can be subject matter of derivatives include equities, bonds, currencies, interest rates and commodities; while derivative variants include options, forwards, futures, swaps and swaptions.

Nigeria being one of the emerging economies in the global financial markets is an exploratory gold mine for derivatives transactions. While the Nigerian derivatives market is still relatively in its infancy and a completely standardised regulatory framework is yet to be fully developed, recent market activities have been geared towards creating awareness and encouraging derivatives trading, with positive results.

Recent developments

The National Association of Securities Dealers (NASD) recently launched an OTC market for the trading of, (among others), derivatives, options, futures, commodities and fixed income instruments. The Financial Markets Dealers Quotation (FMDQ) OTC market also recently launched an OTC market to trade in money market and fixed income instruments. The Nigerian Stock Exchange (NSE) recently announced plans to create an options market that will trade stock options, bond options and indices by Q4 2014, and projects that this will be followed by a futures market that will trade in currency and interest rate futures by 2016.2

With recent and pending development, Nigeria is bound to witness an escalation in the use of derivative instruments in the near future. This chapter examines the enforceability of the netting provisions under the International Swaps and Derivatives Association (ISDA) Master Agreements and highlights existing mitigants for perceived risks, while suggesting proposals for reform.

Derivatives transactions in Nigeria

The Nigerian derivatives market is in a nascent stage, however, Nigerian companies and financial institutions regularly enter into derivatives transactions especially with foreign counterparties. These transactions tend to be documented under the ISDA Master Agreements, which contain extensive provisions on termination, closeout and multibranch netting.

The ISDA Master Agreements typically govern all specific transactions entered into under it, with a single agreement clause designed to preclude cherry-picking by a liquidator. Enforceability of the netting provisions in the ISDA Master Agreements typically requires:

that the netting agreement will be enforceable against an insolvent counterparty and will not be avoided by a liquidator;

that the requirement for calculation of a net sum due from one party to the other will be enforceable;

that the powers of the liquidator to cherry-pick by disclaiming onerous property, contract or transactions while insisting on performance of other contracts will be limited to the net amount due in accordance with the terms of the netting agreement, if at all; and

that any transfer or substitution of collateral will not be considered a preference or fraudulent transfer.

The most fundamental principle of insolvency law in Nigeria is that of pari passu distribution of debt, which means that unsecured debts other than preferential debts rank equally between themselves in winding up. There is currently no legislation or formal rules dealing with termination or closeout netting in Nigeria, therefore termination and/or closeout netting may effectively mean payment of the counterparty’s claims pro tanto ahead of other creditors. However, while the legal requirements to ensure enforceability of netting provisions under the ISDA Master Agreements may not be clear cut, the practicalities are not so far from the ideal.

Avoidance by liquidator

Under Nigerian law, the liquidator of an insolvent company has the right to cherry-pick and may, at any time within 12 months after the commencement of the winding up (or 12 months of the existence of the property coming to the liquidator’s knowledge), disclaim onerous property, contract or transactions.

Payment of a net sum

Nigerian law provides that any disposition of the property of a company, including things in action and any transfer of shares made after the commencement of winding up shall, unless the court otherwise orders, be void.

Nigerian law also provides that where there has been mutual credits, mutual debts or other mutual dealings between a debtor and any other person claiming to prove a debt, an account of what is due from one party to the other in respect of such mutual dealing and the sum due shall be set off against any sum due from the other party and the balance of the account and no more shall be claimed or paid on either side respectively. Mutuality requires the claim and cross claims to be between the same parties in the same right.

A combined reading of the foregoing would suggest that, in the absence of mutuality of claims, the provisions in the ISDA Master Agreement, which provide for the netting of termination values in determining a single lump sum termination amount payable by one party to the other upon the occurrence of an Event of Default or Termination Event may be in contrast with Nigerian law. This matter is however yet to be put to the test in the Nigerian courts.

Preference or fraudulent transfers

Nigerian law also deems as a fraudulent preference (and hence void against the liquidator and other creditors,) any conveyance, payment or disposition of property in favour of a creditor, with a view to giving such creditor a preference over the other creditors, made within three months before the commencement of winding up.

Commencement of winding up

There is no question that the netting arrangements work perfectly well where the netting is completed before winding up. However, issues may arise once a company has commenced liquidation proceedings.

Under Nigerian law, the time for commencement of winding up depends on the mode of winding up. In case of winding up by the court, it is deemed to commence when the winding up petition was presented, and as for voluntary winding up subject to the supervision of the court, it is deemed to commence when the resolution to wind up is passed.

While some legal systems have been able to preserve netting arrangements in insolvency under markets contracts and European Commission derivatives in relation to financial collateral by special statutory provisions in order to reduce systemic risks8, Nigeria currently lacks such statutory provisions.

The need for mitigation of these risks is however not lost on the financial market regulators and as such efforts are being made to address these and other perceived issues that may affect the enforceability of derivative transactions in Nigeria. In the meantime, there are existing risk mitigants available to all or particular counterparties.

Reduction of default risk: Delivery vs payment

Under the Rules and Regulations of the NSE,9 NASD or FMDQ OTC, delivery and settlement is effected on a delivery-versus-payment (DVP) basis. All trades have a three-day settlement schedule (T+3) except for trades in federal and states bonds, which have a T+2, trade cycle.

For exchange traded and OTC derivatives, DVP not only reduces or eliminates default risk by ensuring that a counterparty will give up its securities if, and only if, it receives full payment for them, it also ensures in the case of settlement post insolvency, a liquidator cannot fail to perform its payment obligations while insisting on performance on the part of a counterparty.

Transactions in respect of all counterparties

Given that a liquidator is allowed to disclaim onerous property, contracts or transactions under Nigerian law, while at the same time able to cherry-pick and insist on the performance of favourable contracts, it is worthy to note that a liquidator takes the assets of the company in the same way it finds it. Hence where Automatic Early Termination has been specified to apply, such terms will be enforceable, and a termination value and a net payable sum, possible.

Regarding preference and fraudulent transactions, Nigerian law requires the establishment of a clear intention to prefer one creditor to another. Therefore it is not sufficient to trigger the fraudulent preference provisions by showing a preference, it must be shown that the preference was fraudulent. First, the suspect period is relatively short (three months). Secondly, it may be a bit of a challenge to establish fraud under an ISDA Master Agreement potentially governing several transactions over time.

Transactions in respect of particular counterparties

Derivatives transactions in which the counterparty is a Nigerian registered bank or financial institution may not necessarily suffer from the same challenges faced with ordinary corporates in regard to termination or closeout netting. This is because banks and financial institutions are typically subject to additional administrative procedures prior to the onset of insolvency.

For instance, where a bank informs the Central Bank of Nigeria (CBN) that it is likely to be unable to meet its obligations, or it is insolvent, or where the CBN is satisfied that the bank is in a grave situation as regards to its ability to meet its payment obligations, the Governor of the CBN may give orders as to the management of the bank, and if the CBN considers those steps to be insufficient, the CBN may cede control of the bank to the Nigeria Deposit Insurance Corporation (NDIC).

The NDIC has the authority to remain in control of and carry on the business of the bank until such a time as in the opinion of the CBN that it is no longer necessary for the NDIC to remain in control of the business of the ailing bank.

In the event that the ailing bank cannot be rehabilitated, the NDIC may recommend to the CBN other resolution measures, which may include the revocation of the bank’s licence. Where the licence of a bank has been revoked, NDIC shall apply to the Federal High Court for a winding up order of the affairs of the bank.

Also, an insurance company may only be wound up subject to the approval of the Insurance Commission by not less than 50 policy holders, each of whom holds a policy that has been in force for not less than three years, on the grounds specified in CAMA.

There are additional administrative rehabilitation procedures in place before the commencement of winding up for a bank, other financial institution or insurance company. Therefore, the provisions of the ISDA Master Agreement which defined ‘bankruptcy event’ to include the passing of a resolution for a counterparty’s official management, the appointment of an administrator, conservator, receiver, trustee, custodian or other similar official for it or for all or substantially all of its assets or any event which has an analogous effect to any of the events specified earlier would be sufficient to trigger Automatic Early Termination (where it has been specified to apply) and hence the termination and close-out netting provisions before the commencement of such counterparty’s insolvency.

CONCLUSION

From all indications, derivatives will continue to be used as a tool for risk reduction and efficient portfolio management. As Nigeria positions itself to take advantage of the benefits of these dynamic financial instruments, it may be useful to develop a legal structure that enhances the enforceability of derivative transactions in Nigeria through the enactment of an enabling law. Such a law should, at the very least ensure:

that derivative transactions shall not be deemed to be unenforceable by reason of gaming, gambling, wagering or insurance laws; and

that netting agreements will be enforceable against an insolvent counterparty and will not be avoided by a liquidator, be considered a preference or otherwise rendered unenforceable by mandatory insolvency laws.

The Nigerian financial market regulators are aware of this and with the Securities and Exchange Commission actively driving the establishment of an enabling legal framework for derivatives transactions in Nigeria, we expect that any current perceived legal issues will be addressed soon.

Liquid Telecom Buys Neotel, Will Become Largest Pan-African Broadband Network

Liquid Telecom, a privately owned, pan-African telecoms group, majority owned by Econet Wireless Global, said it has agreed to acquire South African communications network operator Neotel for ZAR6.55 billion (about $428 million USD), according to a recent Forbes piece.

Liquid Telecom is partnering with Royal Bafokeng Holdings (RBH), a South African investment group, which would take a 30 percent equity stake in Neotel. Neotel is currently majority owned by India’s Tata Communications (Tata Communications Limited (ADR) (OTC: TTCMY)).

The deal will create the largest pan-African broadband network and B2B telecoms provider.

In a press release, Liquid Telecom said “businesses across Africa will be able to access Liquid Africa’s 24,000km of cross-border, metro and access fibre networks. These currently span 12 countries from South Africa to Kenya, with further expansion planned.”

However, the Forbes coverage cited the networks as being “40,000kms of cross-boarder, metro and access fibre networks.”

“We are excited about this transaction. Leveraging the strengths of RBH, Neotel and Liquid Telecom will offer an unprecedented fibre network with a unique set of services and international connectivity for telecom operators and enterprises across sub-Saharan Africa,” Nic Rudnick, Liquid Telecom CEO, said in a statement.

Subject to approval by South African regulatory authorities, the deal is expected to be completed later this financial year.

Nigeria is finally going to do the painful thing everyone said it has to do

Business Insider/ Nigeria is finally going to do the painful thing everyone said it has to do.

The central bank announced on Wednesday that the naira peg will be abandoned on Monday, June 20, and the currency will be allowed to float freely.

Although, Central Bank of Nigeria Governor Godwin Emefiele also said that the bank will intervene “as the need arises.”

As for what this means for Nigeria’s economy, in the short-term it’s going to get ugly. But in the long-term, things should start to pick up.

“Over the long-run, a weaker currency will help Nigeria’s economy by encouraging import substitution and attracting foreign investors, who have shunned the country for fear of a devaluation,” wrote Capital Economics’ Africa economist John Ashbourne in a note.

“But the move will be painful over the short term. Higher import prices will add to inflation, which reached 15.6% y/y in April. This will probably force the authorities to tighten monetary policy,” he added.

Plus, if Nigeria’s central bank can’t get inflation back under control, then the country might end up getting stuck in a “vicious” cycle of high inflation that leads to a weaker naira, noted Marc Chandler, the global head of currency strategy at Brown Brothers Harriman. And that, then, could lead to higher inflation.

“This is one reason why devaluations can be so painful, as central banks typically jack up interest rates afterwards. Recessions are often seen post-devaluation,” he wrote. “Yet if Buhari has finally relented on maintaining what we viewed as an unsustainable peg, the longer-term outlook for Nigeria will have improved.”

Analysts have long been arguing that Nigeria will eventually have to capitulate and devalue its currency given that the government’s controversial agenda of currency and price controls created a bunch of economic stresses in Africa’s largest economy. Most recently, inflation soared to a six-year high.

Still, devaluing the currency peg will not magically fix all of Nigeria’s problems.

The country continues to suffer from numerous headaches, including lower oil prices, the fuel-shortage crisis, and ongoing oil-production disruptions by the Niger Delta Avengers. Plus, the Nigerian Bureau of Statistics recently revealed that the country’s economy shrank by 0.4% year-over-year in the first quarter, which was way worse than expected.

“A weaker currency is, at best, a necessary but insufficient condition of an economic recovery,” concluded Ashbourne.

But at least it’s a step in the right direction.

Nigeria: Niger Delta Avengers Threaten Further Violence in Oil-Producing Region

The Niger Delta Avengers (NDA) has warned Nigerian authorities it may “review our earlier stance of not taking lives” if oil companies continue to operate in the country’s oil hub.

The militant group has launched a series of attacks on oil pipelines and facilities in the Niger Delta, where the majority of Nigeria’s oil reserves are concentrated. The NDA has so far rejected offers of dialogue from the Nigerian government and vowed to continue its Operation Red Economy, the purported goal of which is to reduce the West African country’s oil production to zero.

In a statement published on its website on Monday, the NDA said that the oil companies must not carry out any repair works on the affected pipelines and that buying of crude oil from the Niger Delta must be suspended “as we await the right atmosphere that will engender genuine dialogue.”

The NDA has claimed attacks on facilities belonging to several international oil companies, including Royal Dutch Shell, U.S. firm Chevron and Italian oil giant ENI. Some of their attacks have shown a high degree of sophistication and have taken down strategically-important pipelines—the first attack claimed by the group was on an underwater pipeline at Shell’s Forcados terminal and forced the company to temporarily shut down the 250,000 barrels per day (bpd) terminal.

Nigerian oil minister Emmanuel Ibe Kachikwu attempted to reach out to the militants earlier in June, saying that the Nigerian military would step back from pursuing the group in order to establish a platform for dialogue. In Monday’s statement, however, the NDA said it would only participate in dialogue with “independent mediators” appointed by the international oil companies working in the region.

Historically, the Niger Delta has been the site of previous uprisings by militant groups, who have claimed that the impoverished region does not benefit sufficiently from its oil wealth. In the mid-2000s, militants led by the Movement for the Emancipation of the Niger Delta (MEND) decimated the country’s oil production and kidnapped oil workers, with the insurgency only coming to an end in 2009 with the introduction of an amnesty program for the fighters. MEND has publicly called upon the NDA to engage in dialogue with the government, but the latter group has rejected the former and criticized its leaders for abandoning their cause.

Largely as a result of attacks by the NDA and other militants, Nigeria’s oil production has plummeted from 2.2 million bpd to a 20-year low of between 1.5 million and 1.6 million bpd.

Inflation is getting out of control in Africa’s largest economy

Business Insider – Africa’s largest economy is failing to keep inflation under control. Nigeria’s inflation accelerated to 15.6% in May, up from 13.7% in the previous month, according to the National Bureau of Statistics.

That’s the highest rate in over six years, and above economists’ expectations of 14.7%.

The continued rise in Nigerian inflation over the last few months has been attributed to the government’s controversialagenda of currency and price controls, including on petrol.

Nigeria has attempted to hold its currency, the naira, fixed at 200 per dollar on the official FX market by rationing the supply of dollars. So, as a result, consumers have been trying to get dollars from the parallel market, where the exchange rate was 320 nairas per dollar, according to March figures.

As for the second policy, Nigeria attempted to fix the retail cost of petrol at 86.5 nairas per liter, which has resulted in one of the worst fuel shortages in years.Petrol prices on the black market and other utility prices have, unsurprisingly, skyrocketed in the aftermath.

“Given that both the naira policy and the petrol pricing strategy were originally presented as methods of keeping prices down, the continued rise of inflation is a significant blow to the government’s economic strategy,” Capital Economics’ Ashbourne noted previously.

On the positive side, in late May, the government finally admitted that it needed a more flexible exchange rate. And there have recently been reports that the Central Bank of Nigeria is thinking about introducing a dual exchange-rate system and devalue its currency.

But, for now, “today’s data underline the failure of the current FX system to keep inflation under control,” according to Ashbourne.

Property sales in Lagos, Abuja thrives despite fiscal austerity

International Guardian, Houston – TX- Amidst market skepticisms over its strict fiscal management of the economy, property sales in Nigeria’s two major cities, Lagos and Abuja might not be as bad as being perceived, according to the Chief Executive of Keeraa Koncept Properties & Real Estate Investments, Ms. Joy Nwabunike. In a paper presented to a consortium of Nigerians in the Diaspora seeking property acquisition and development back home, Ms. Nwabunike admitted that the Nigerian real estate sector had been dogged by the on-going foreign exchange crisis, but stated that individuals self-financing their investments or paying cash still thrives with specific benefits.

“A lack of mortgage financing and cost of funding may have drastically prevented effective demand in both commercial and residential housing market, and this has also led to reduction in prices. The advantage is that this abnormal market environment benefits those buying with cash,” she said. With the Dollar rising crushingly against the Naira, Ms. Nwabuike indicated that prospective buyers living abroad stands the opportunity to invest in affordable housing and commercial properties. “Most of our prospective buyers now are those living outside the country,” Ms. Nwabunike said.

Currently, Nigerians living abroad are most likely to invest in real-estate than automobile and consumer goods, International Guardian investigations reveal. “Things are so hard now that people hardly spend money buying cloths, perfumes, and computers,” noted Paul Ndubuaku, a Texas-based merchant who normally procures assorted consumer goods and sells in Nigeria. “It is frustrating when you carry those items home and have to sell them off because people are not buying. I am actually looking into rental properties, or may be commercial properties in Abuja – depending on costs and the area,” he said.

UPSCALE and AFFORDABLE HOUSES in NIGERIA ■ Beautiful Houses for sale in Lagos and Abuja Area; Enquiries, Click >>>>>>>

Ndubuaku told International Guardian that he was already looking at two properties in Dawaki and Maitama extensions in Abuja respectively. Buying houses through individuals and acquaintances could be risky because of process regulations and documentations. Ms. Nwabunike noted that there were many attractive properties within and outside Abuja, but advised prospective buyers, especially those living outside Nigeria to seek the help of credible real estate companies to avoid service complexities.

Delta Avengers reject Nigeria talks, blow up Chevron site

ABUJA (Reuters) – The Niger Delta Avengers militant group on Wednesday rejected an offer of talks with the government to end its attacks on oil facilities and said it had blown up a Chevron pipeline site in the Niger Delta.

Attacks by militants on oil and gas pipelines in the southern delta swamps have brought Nigeria’s oil output to a 20-year low and helped push oil prices to 2016 highs.

Nigeria’s oil minister said on Tuesday the government would start talks with the Niger Delta Avengers, which has claimed responsibility for a string of attacks in the delta.

The militant group rejected the offer of talks on its Twitter account. “We’re not negotiating with any committee,” the group said. “If the Fed Govt (federal government) is discussing with any group they’re doing that on their own.”

The group said it had blown up a Chevron site called “RMP 20” located next to the Dibbi flow station in the Warri area in the delta at 0100 local time. It has previously attacked Chevron, Shell and ENI facilities.

An RMP, or remote manifold platform, is a gathering location where small oil or natural gas pipelines converge before connecting to a larger storage hub. It is not a producing well, though the Niger Delta Avengers have conflated the two terms in posts on social media and other platforms.

“The attack on Chevron’s RMP 20 is confirmed,” said local community leader Chief Godspower Gbenekema. “The place is on fire.”

Chevron, citing long-standing policy, declined to comment.

“We do not comment on the safety and security of our personnel and operations,” Chevron spokesman Kent Robertson said.

While Chevron is the third-largest oil producer in Nigeria, its biggest production streams are offshore, which has mitigated the immediate impact on oil output from the spate of attacks on its infrastructure.

A group of former Niger Delta militant leaders issued a statement on Wednesday condemning the actions of the Avengers and urging them and other groups to “re-consider their activities.”

“We enjoin our brothers to give peace a chance, lay down their arms and accept the offer for a meaningful dialogue,” said the Leadership, Peace and Cultural Development Initiative.

(Reporting by Ulf Laessing in Abuja; Additional reporting by Tife Owolabi in Yenagoa, Anamesere Igboeroteonwu in Onitsha, Libby George in London and Ernest Scheyder in Houston; Writing by Ulf Laessing and Alexis Akwagyiram; Editing by William Hardy and Leslie Adler)

Nigeria Without Oil: Focusing on the Fundamentals

Lagos, the economic capital….Nigeria has the largest population or domestic market.3 Almost in a bid to spite the rest of the world, in addition to the above resources, providence spared Nigeria from significant natural disasters.By Patrick O. Okigbo III

Permit me to tell you a story of a prodigal entity that squandered its wealth on frivolities and, now it appears that the music is over. It now needs to decide on how best to return to the basics and ensure its very survival. There are no easy choices. The question, therefore, is whether Nigeria has what its takes to make big, difficult, decisions.

Share the Wealth

There are a few countries in the world that are as blessed as Nigeria. Only 8 countries have more arable land than Nigeria.1 Nigeria has over 40 different types of precious minerals2 and floats on a sea of natural gas and crude oil. But for six countries, Nigeria has the largest population or domestic market.3 Almost in a bid to spite the rest of the world, in addition to the above resources, providence spared Nigeria from significant natural disasters.

But, on its own, Nigeria over time adopted a severely destructive strain of corruption. With the discovery of oil in commercial quantities, the country lost its thrift and discipline, and adopted prodigality. The World Bank estimates that over $400 billion of oil revenues has been stolen or misspent since 1960

But, on its own, Nigeria over time adopted a severely destructive strain of corruption. With the discovery of oil in commercial quantities, the country lost its thrift and discipline, and adopted prodigality. The World Bank estimates that over $400 billion of oil revenues has been stolen or misspent since 1960. Furthermore, Nigeria has received over $400 billion in aid. The combined amount is equivalent to twelve times what the United States pumped into reconstructing the whole of Western Europe after World War II.4

The perfect storm

But it appears the music may have stopped as Nigeria now finds itself in a perfect storm. There has been a significant decline in oil revenue, which accounts for over 80 percent of Nigeria’s budget. The Civil Services are largely unproductive and can’t think Nigeria out of its current economic malaise. The 1.2 million Nigerians who are not able to gain admission in universities every year remain semi-literate. The 0.5 million graduates who enter the labour market every year are not much better. Furthermore, Nigeria failed to invest in economic infrastructure when oil revenue gushed. It succeeded in creating a political class that spends more time scheming their way to the feeding trough and spares little thought to economic development or the improvement of the lives of its citizens.

In the face of these challenges, Nigeria’s gross domestic product dropped from a high of 7 percent over the last 10 years to negative 0.36 percent in Quarter 1 of 2016. By the end of June 2016, Nigeria will be officially in a recession. Nigeria will be in an economic recession as it prosecutes a war in the Northeast, potentially another war in the South- South, while the Biafran agitators in the Southeast continue to rattle the cage.

Petroleum sector analysts estimate that price recovery to $100 a barrel will take over two decades. This puts Nigeria’s finances in a shambles. The situation is worsened by states that are proving to be economically unviable. Most of the states in Nigeria are unable to pay their staff salaries and continue to rely on bailouts from a Federal Government that may soon need a bailout. Every thing seems to be falling apart: electricity, education, healthcare, transport infrastructure, security and the socio economic indicators.

There is enough prescriptive literature on the economic sectors Nigeria should focus on. The current administration is already prioritizing agriculture, solid minerals, power sector, etc. The challenge with these recommendations is that there is usually no consensus on the economic objectives and methodology for selecting the sectors.

Time to go home

Like the biblical prodigal son, Nigerians realise that the country cannot continue on this trajectory of sub-optimal performance. The challenge, however, is how to reach a decision on the most optimal options for Nigeria.

Most commentators propose the diversification of the economy away from an over-dependence on the petroleum sector. That is where the consensus ends.

The Nigerian economy is quite diversified with services contributing about 56 percent of the GDP, industry contributes about 24 percent, and agriculture contributes about 20 percent. The question, therefore, is how can Nigeria develop these sectors (that are already contributing to GDP) to increase their contributions to funding the budget? Petroleum revenue contributes about 85 percent.

The Options

There is enough prescriptive literature on the economic sectors Nigeria should focus on. The current administration is already prioritizing agriculture, solid minerals, power sector, etc. The challenge with these recommendations is that there is usually no consensus on the economic objectives and methodology for selecting the sectors. Late last year, principals from my firm, Nextier Advisory, were involved in an exercise to prioritize economic sectors to promote foreign direct investment. We made the assumption that government’s priority is to create jobs for the millions of young Nigerians. This goal was gleaned from the speeches and public pronouncements of the government. We used a methodology that evaluated 55 economic sub-sectors by attractiveness and feasibility. Attractiveness was measured using two parameters: size of the opportunity and impact on job creation, while feasibility was measured using Nigeria’s ability to compete against other countries in sub-Saharan Africa, and the ease of removing constraints to foreign direct investments. The result of the analysis was a bit surprising.

The top five sectors were Business Process Outsourcing, Automotive, Cassava, Renewable Energy, and Packaging. This is where the good news ends and the gory story begins. Nigeria has always been very good at producing strategy documents but not necessarily good ideas. At Nextier, we define “good ideas” as those solutions that take full account of the opportunities as well as the challenges and obstacles to their full implementation. Most of the strategy documents do not focus enough effort on the reasons why we have never been able to implement and then propose how best to\ navigate the implementation process.

How did we get here?

An Igbo adage states that one who does not know where the rain started beating him will not know where the rain stopped pelleting him. If we do not seek to understand how Nigeria got in to this mess in the first place, we will not figure out how to get out of it. So when did the wheels of

Nigeria begin to wobble?

We can go all the way back to 1914 and rest the blame at the feet of the colonial masters but after 100 years, we would be challenged to find anyone who would truly agree with that assessment. We must cast our gaze much closer to the 1960s. Nigeria had the misfortune of military intervention only 6 years into self-rule. The military, which could be excellent at what they have been trained to do, are not the greatest candidates for nation building. In the 28 years they ruled Nigeria, they appeared to wage a war against intellectualism and empowered apologists who did not understand the tenets of economic planning and nation building. These apologists became the politicians of the postmilitary era. These politicians begot other politicians of their ilk and we have continued this dive to the bottom of anti-intellectualism. Today, what we have is a public space that is dominated by people who should have nothing to do with piloting the affairs of state. A good friend of mine put it quite succinctly, “those who speak for us today, are the one who should sit with paper and pen in hand and simply take notes. Those who should speak have been chased away from the public space”. It is therefore not surprising that we are not able to marshal the intellectual power required to solve some of our most banal problems.

Nigeria Without Oil: Focusing on the Fundamentals

This lack of competence pervades Nigeria’s public service. The depth of the incompetence is staggering. Can our Civil Service deliver the policies, programmes, and implementation required to deploy the infrastructure that will support 480 million Nigerians by 2050? Can this Civil Service compete against a rising China and India? It is clear to any casual observer that we lack what it takes to pull Nigeria out of the current economic quagmire. At what point do we stop scratching with chickens and start soaring like eagles?

But after 17 years of civilian rule, we are wasting time casting the blame on the military. The blame has to rest squarely at the feet of the Peoples Democratic Party that was in power for those years. While there is much to be celebrated in the economic reforms of the Obasanjo years that resulted in almost a decade of 7 percent GDP growth, and the infrastructure development of the Jonathan years, there is much that is left to be desired. It is the public service that will develop the policies and implement the programmes. A reform of the Civil Service should have been top priority for the government.

Time to go home

For Nigeria to be able to diversify its revenue base, it must create the impetus for reform, decide on the economic goals and enablers, prioritise the sectors, develop good ideas, focus on implementation, and manage the results.

Create the impetus for reform

We can’t assume that everyone understands that the cavorting is over. For instance, the State governments can’t pay salaries but we are yet to see any commitment to fundamental restructuring of governance. Nigeria Without Oil: Focusing on the Fundamentals Remember that some state governors opposed the Sovereign Wealth Fund (in the name of opposition politics) and also of these same governors put pressure on the Federal Government to draw down from the Excess Crude Account even before the rainy day. Furthermore, it appears that the Labour Unions do not quite understand how bad things and that is the reason why they oppose efforts to right size.

Decide on the economic goal(s) and enablers

There are a number of complimentary economic goals that the government can focus on: job creation, economic growth, income equality, quality of life, etc. However, there is need to secure consensus and sequence these economic goals to agree on the optimal economic development strategies.

There are a number of enablers of a fully diversified revenue base for Nigeria. These enablers include governance structures for improved transparency and accountability; public service reforms, enabling economic infrastructure, etc. Take infrastructure, for instance, Nigeria needs $65 billion to meet the commitment for infrastructure development over the next five years. In all, Nigeria needs $2.9 trillion over the next 30 years.

Prioritise the sectors Nigeria does not have the ability to invest in all economic sectors. As a result, it must prioritise. This focus also helps with efforts to promote foreign direct investment to the sectors. This point is more apt given the steady decline in Foreign Direct Investment from 2012.

Ideas.

The failure of Nigeria is the failure of the intelligentsia. The politicians are good at what they do: the win power by any means possible. The intellectual class has not been as effective. The intelligentsia should think through the challenges of implementation and present a plan that the politician can simply approve and facilitate implementation.

While Nigeria has a library of policy documents and strategies, the fact that these plans have not yielded the desired results is indicative that the ideas may not have been well considered. These documents should have considered the evident challenges and proposed a way to side step and navigate them. Therefore, any ideas that are proposed today for diversifying Nigeria’s revenue base should be subjected to rigorous scrutiny and debate. They must be based on verifiable methodologies and data. Anything short of this is simply a work of fiction and should be considered as such.

Implementation.

The bitter nugget of truth is that Nigeria lacks the capacity to implement. Our recent history shows that our human capital is not up to par. This assessment is not to castigate; rather, it is to highlight the need for a new approach to implementation. Dubai was a country of pearl divers when they discovered oil. Knowing that they lacked the human capital to deliver their vision, they bought the required experience and got the job done. We are getting to a point where we may begin to think about such models.

Results.

It appears that what we have in Nigeria today is government by “strategic communications”. Government spends a lot of time celebrating what it plans to do and not what it has done. Government decisions should be driven by data, and not propaganda or politics.

A review of Nigeria’s Federal and State budgets shows a lot of projects that are funded without any assessment of performance or delivery. Every year, more funds are assigned to such programmes because they are already on the previous year’s budget without assessing their feasibility or measuring their impact. A nation that fails to measure and calibrate is bound to deliver sub-optimal results.

Bringing it together

The real question is not whether Nigeria is willing to diversify its revenue base because, let’s face it, Nigeria does not have a choice but to diversify or else we will be like Venezuela. This is not the time to play partisan politics with this issue. This is not the time to be PDP or APC or XYZ. This is the time to be NGR – Nigerian. Every Tomi, Dike, and Haruna must shelf his or her historical biases to realise that we are all in this Titanic together and it has already hit the iceberg. We can sit on deck and twiddle our fingers, pray, and hope that by some miracle the gaping hole with close. Or we can roll up our sleeves, forget our differences, focus on our commonalities, and fight together because we will either win together or we will all die together.

Patrick O. Okigbo III is the Principal Partner at Nextier Advisory – a multi-competency public sector advisory firm with expertise in research, strategy, finance, monitoring and evaluation, and strategic communications.